Originally, the following article was ready to publish in January, just before the U.S. House passed HR 7024, which included a fix for the 280C election discrepancy in the Form 6765 instructions. In the legislation under Section 201, paragraph (f) Transition Rules (4) “Election Regarding Coordination with Research Credit,” the Bill would allow a taxpayer to file an amended return to make a 280C election or revoke a previous election made on the 2022 return.

Now that it is May and looking less likely the Bill will be passed by the Senate any time soon, I ask that you read and consider the following.

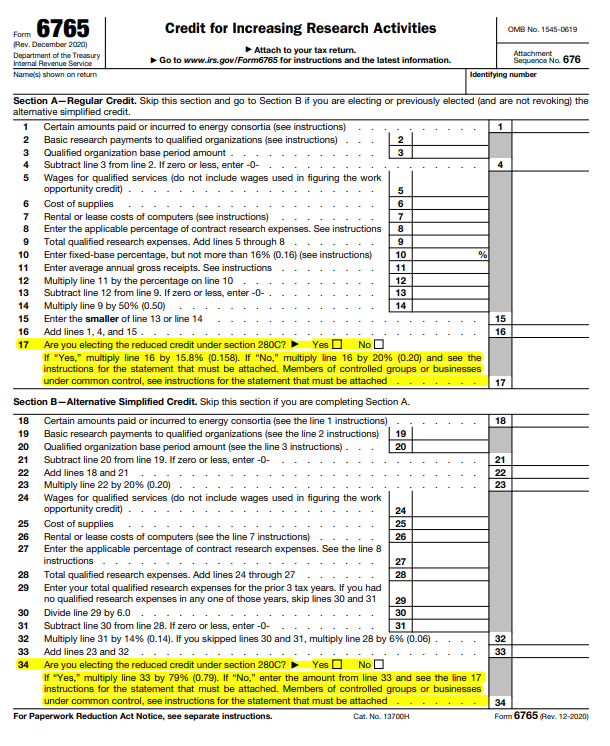

If you filed Form 6765 to claim the research credit for 2022, and you checked the 280C box YES on line 17, then I would like to hear from you. Why did you elect the reduced credit? Did you make a mistake? Were you following the form instructions? Were you aware you probably didn’t need to make the election?

Erroneous Form 6765 Instructions

Form 6765, line 17 (line 34 for the ASC method), requires taxpayers to check the box to elect the reduced credit under section 280C, to avoid having to reduce research expenses by the amount of the credit. Before last year, most taxpayers made the election and didn’t think twice about it. It allowed you to claim a smaller credit without reducing any expenses, which would have increased taxable income and potentially impacted state return filings.

The Form 6765 instructions (revised January 2023) contained the following sentence related to lines 17 and 34: “If you don’t elect the reduced credit, you must reduce your otherwise allowable deduction for qualified research expenses or basic research expenses by the amount of the credit on this line.”

The unfortunate thing about those instructions is that they were old and applicable to tax years before 2022 and should have been revised after recent law changes.

Nowhere in the instructions, including the “What’s New” section, was there mention of a crucial change to the law, explained later. The law changes should have been highlighted under “What’s New” with a cautionary note to taxpayers about checking the box on lines 17 or 34 to elect the reduced research credit, and the sentence should have been removed from the instructions or rewritten. The instructions were incorrect; if you followed them, you likely unnecessarily reduced your research credit. Thus, the reason for this article and request for taxpayers to email me. I would like to help you by encouraging the IRS to allow taxpayers who unnecessarily reduced their credit by following the instructions to revoke their 280C election!

Changes to IRC §280C(c)

Public Law 115-97 Dec 22, 2017, 131 STAT. 2112, Sec. 13206, changed IRC §174 and §280C(c), effective for tax years beginning after December 31, 2021. Taxpayers could no longer deduct expenses under §174. Under the revised statute, expenses must be capitalized and amortized over five or fifteen years. Congress also made a corresponding change to §280C(c) by repealing the following language: “In general, no deduction is allowed for that portion of the qualified research expenses (as defined in I.R.C. § 41(b)) or basic research expenses (as defined in I.R.C. § 41(e)(2)) otherwise allowable as a deduction for the taxable year that is equal to the amount of the credit determined for such taxable year under I.R.C. § 41(a).” Before dropping this provision, a taxpayer was required to reduce their otherwise deductible expenses by the amount of the research credit unless an irrevocable election was made to reduce the credit.

IRC §280C(c)(1) now states, “In general, if the amount of the credit determined for the taxable year under section 41(a)(1), exceeds the amount allowable as a deduction for such taxable year for qualified research expenses or basic research expenses, the amount chargeable to capital account for the taxable year for such expenses shall be reduced by the amount of such excess.” Since the amount of research credit would seldom ever exceed the amount of the amortization on the capitalized expenses, a taxpayer would not be required to reduce their credit and therefore would not make a §280C(c)(2) election to reduce their credit.

Making the election permanently reduces a taxpayer’s research credit since the election is irrevocable, as stated in §280C(c)(2)(C). I do not believe taxpayers have any current recourse, which is very disappointing. Since the election is statutory, the only possible relief would have been the automatic extension under § 301.9100-2(b); however, this section only allows for a six-month extension from the filing due date. So, if a taxpayer filed their return by the extended due date, any benefit from the extension would have expired. Also, it seems to allow only for making an election, not revoking it. The irony is that the statute was enacted to prevent taxpayers who did not make the election on their original return from making the election later, not preventing a taxpayer who made the election in error from revoking it later.

What To Do If You Made an Unnecessary Election:

I personally know of three taxpayers who have fallen into the trap of an unnecessary election. I have been in contact with the IRS, and options for these taxpayers appear to be limited. The Advocate’s Office seems unable to help, and IRS Policy is reluctant to consider any action, not knowing how many taxpayers have been affected.

If you or one of your clients has this situation, please contact me at [email protected], and I will continue pursuing a potential resolution.

September 25th

3:00 pm EST