The new Section G of Form 6765 is where the IRS gets serious.

It’s no longer enough to calculate your Qualified Research Expenses (QREs) and report a total. The IRS now expects detailed, project-level reporting that ties expenses to specific business components, categorized and ranked.

If your tax team doesn’t understand how Section G works—or how to fill it out correctly—you risk refund denials, audit exposure, or outright rejection.

Here’s what every enterprise tax team needs to know.

What’s New in Section G?

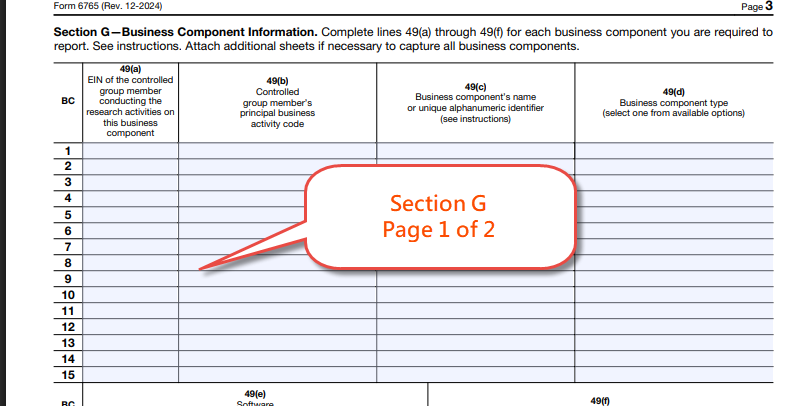

Section G introduces a more structured format for reporting R&D activities:

- You must report up to 50 business components that account for at least 80% of total QREs.

- For each business component, you must report:

- Type of component: product, process, software, technique, formula, or invention

- Wages, supplies, and contract research costs

- Job function split for wages (Direct, Supervisor, Support)

- Components must be listed in descending order of QRE value.

This isn’t just a formatting update—it’s a shift in how the IRS wants to evaluate R&D tax credit eligibility.

Why This Section Matters More Than Ever

Section G is now the most detailed and compliance-sensitive part of the form. It’s where your claim gets made—or challenged.

- If you can’t clearly define business components or connect them to documented research activities, your claim is vulnerable.

- If your totals don’t align with underlying documentation, the IRS may view the claim as unsubstantiated.

- If your classification is vague or inconsistent, it raises red flags.

In short: this is where the IRS will look to validate—or reject—your study.

How to Fill Out Section G the Right Way

To accurately complete Section G and avoid unnecessary IRS scrutiny, your team must prepare with precision and consistency. Here’s how:

- Begin by identifying your top 50 business components, sorted by total QRE value. Focus on real, defined R&D activities rather than generic groupings like “Platform Development.”

- For each business component, link to detailed documentation that supports the four-part test: show the uncertainty being addressed, what was tested, how it was tested, and the results.

- Break out costs precisely. Wages should be allocated by job function (Direct, Supervisor, Support) and tied back to each component. Use expense reports, time tracking systems, or project costing data where available.

- Apply a consistent format and structure. Use naming conventions, project codes, and templates that streamline reporting and ensure consistency across departments and years.

- Before you file, validate that the top 50 components account for at least 80% of your total QREs. Also confirm that each one meets the Process of Experimentation (PoE) standards required by the IRS.

Final Thoughts: Section G Is Where the Details Matter

The IRS created Section G to raise the bar on substantiation—and it’s working.

Make this section the strongest part of your filing, not the weakest. If your tax team can align costs, documentation, and R&D strategy in Section G, you’ll not only survive audit scrutiny—you’ll set a defensible precedent for future claims.

Schedule a consultation with MASSIE today.

September 24, 2026

2:00 pm EST