This article was originally prepared for release in January, just before the U.S. House passed HR 7024. That bill included a fix for the 280C election discrepancy in the Form 6765 instructions. Under Section 201, paragraph (f) Transition Rules (4), the legislation would allow a taxpayer to file an amended return to make a 280C election—or revoke a previous election—on their 2022 return.

Now that it is May, and with the Senate unlikely to act soon, it is worth reviewing what went wrong.

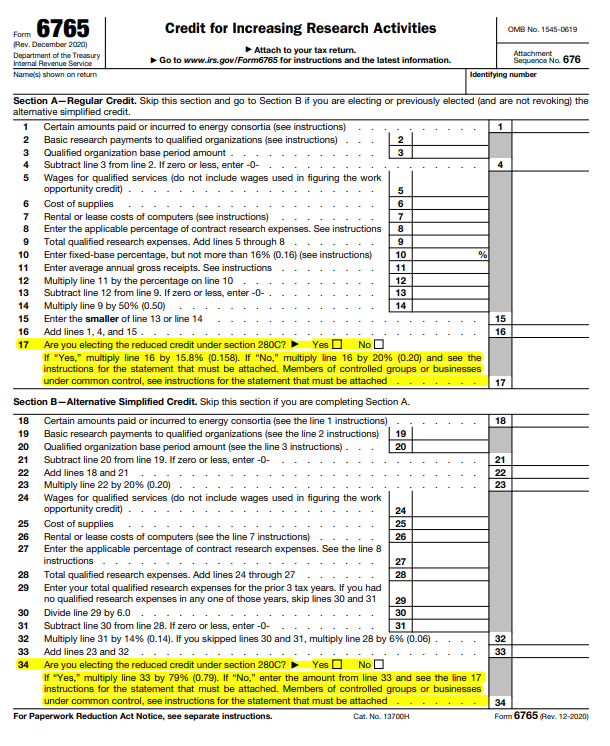

The Impact of Checking the Box

If you filed Form 6765 to claim the research credit for 2022 and checked the 280C box on line 17, you may have reduced your credit unnecessarily. Many taxpayers did so because the instructions seemed clear at the time. But were you aware that you probably didn’t need to?

Erroneous Form 6765 Instructions

Form 6765, line 17 (or line 34 for ASC), requires taxpayers to check a box to elect the reduced credit under Section 280C. This avoided reducing research expenses by the credit amount, which would have increased taxable income and potentially impacted state filings.

The instructions revised in January 2023 still said:

“If you don’t elect the reduced credit, you must reduce your otherwise allowable deduction for qualified research expenses or basic research expenses by the amount of the credit on this line.”

That guidance was outdated. It applied to tax years before 2022, not after. The “What’s New” section failed to warn taxpayers about the change in law. The IRS should have revised the instructions, or at least flagged the issue. Because it did not, many taxpayers checked the box and permanently reduced their credit.

Changes to IRC §280C(c)

The problem stems from changes in the 2017 Tax Cuts and Jobs Act (Public Law 115-97). Effective for tax years beginning after December 31, 2021, Congress amended IRC §174 and §280C(c). Under the new rules:

-

Research expenses must be capitalized and amortized over five or fifteen years.

-

Congress repealed the requirement to reduce deductions by the research credit unless the taxpayer elected the reduced credit.

IRC §280C(c)(1) now states that if the credit exceeds the allowable deduction, the amount charged to capital must be reduced. But in practice, the credit almost never exceeds the amortization amount. That means taxpayers no longer need to make the election.

Unfortunately, if you did make it, the election is irrevocable under §280C(c)(2)(C). Once made, it permanently reduces your research credit.

Limited Avenues for Relief

Because the election is statutory, recourse appears limited. The automatic six-month extension under §301.9100-2(b) applies only for late elections, not for revoking elections made in error. Even worse, the IRS enacted the rule to stop taxpayers from making late elections, not to penalize those who followed outdated instructions.

I know of at least three taxpayers who fell into this trap. I’ve contacted the IRS, but options are slim. The Advocate’s Office cannot help, and IRS Policy has hesitated to act without knowing how many taxpayers are affected.

What You Can Do Now

If you or a client checked the 280C box in 2022 based on the instructions, your claim may be at risk. I want to continue raising this issue and pushing for a remedy. Please contact MASSIE’s Director of Controversy, Steve Whiteaker, at [email protected] if you are in this situation.

June 24, 2026

2:00 pm EST